Yahoo!: Declining Business or Evolving Company?

Printer Friendly

Printer Friendly

Yahoo (YHOO) has recently garnered a lot of attention from investors mainly because of its stake in Alibaba (BABA). Yahoo is one of the world’s largest internet corporations, mostly recognized for its web portal, search engine and email service, but has become what can be called a declining business. However its rather successful investment in Alibaba has boosted its standing and has subsequently opened up a lot of possibilities for Yahoo’s future as a company.

Yahoo has seen a significant increase in share price over the last 2 years jumping from an initial price of $18 to today’s current price of $52.17 (shown below).

Most of the stock’s appreciation can be accredited to Yahoo’s position in Alibaba, but hiring CEO Marissa Mayer has not hurt either and its most recent jump from the low $40s to the $50s can be attributed to Yahoo’s recent gain of $8.3 billion (before taxes) from the selling of 120 million shares of Alibaba stock. There is a lot of speculation on what Yahoo will do with its excess cash and at the same time, there are a lot of questions concerning Yahoo’s overall value as a company and its future prospects.

Contents

Proceeds from Alibaba: What are Yahoo’s plans?

First and foremost, Yahoo has already promised investors that they would share in half the proceeds from Alibaba’s IPO in some way (stock buybacks), so we have some sort of idea as to what Yahoo plans to do with the $6.3 billion (after taxes). Furthermore, we already have an idea as to what CEO Marissa Mayer has planned for Yahoo from her past two years of leadership: Yahoo acquired a total of 26 companies in 2013 for approximately $1.3 billion, with social blogging site Tumblr being its largest purchase at $1.1 billion. There is no clear strategy among the acquisitions that Mayer has targeted, in that the companies seem to be all over the map as far as markets served. Many investors are questioning whether Mayer’s plan is feasible. Some have speculated that a there is a pattern in Mayer’s sporadic purchasing of startup companies, suggesting that she is targeting companies she believed would not only bolster Yahoo’s advertising functions, but also add long-term value to its mobile platform. Yahoo’s acquisitions have showed results that are less than stellar so far, with Tumblr and many other companies still being in the red. Mayer claims things will begin to pick up hopefully in 2015 as her strategy slowly unfolds, so ultimately the jury is still out.

I believe that Yahoo’s most recent acquisition of BrightRoll for $640 million, its largest purchase since Tumblr, is, however, a worthy investment because BrightRoll would add significant value to Yahoo’s core operations. BrightRoll, a large video advertising firm, is a large growing business whose revenue is expected to surpass $100 million this year. The acquisition would also allow Yahoo to add video to the suite of display, native, and mobile ads that it is offering marketers. It is expected to “dramatically strengthen Yahoo’s video advertising platform, making it the largest in the US,” according to Mayer.

I also thought about what kinds of companies Yahoo could acquire in the future to add significant value to its business. While researching, I discovered it was a general consensus that AOL would be the optimal choice due to both high synergy between the companies and high costs savings if the two were to merge. If this merger does happen, then the results would be extremely beneficial for Yahoo—this Seeking Alpha article takes a deeper look.

Yahoo also reduced the initial amount of Alibaba shares it was required to sell during the IPO by 47%, from 262 million to 140 million, allowing them to keep approximately 383 million shares of Alibaba, which was a very smart move on Mayer’s part, as it essentially gave her more time to realize the strategy she has been trying to implement. Most of Yahoo’s value stems from its investments in Alibaba and Yahoo Japan (I explain this more in the next section), so sitting on these investments and letting them grow will in turn cause Yahoo’s stock to appreciate as well. Management’s main goal here is to satisfy shareholders by giving them short-term results through Alibaba and Yahoo Japan while trying to grow the core revenue drivers of Yahoo.

Most recently, Mozilla Firefox announced a new five-year deal with Yahoo where it will dump Google for Yahoo and convert its default search system to Yahoo which strengthens Yahoo’s search capabilities, increasing the total advertising space available for purchase. Tech data firm, StatCounter, estimates Firefox still has a 10.4% combined PC/mobile/console browser share globally. Things are starting to pick up for Yahoo and if Mayer’s strategy, if she does indeed have one, takes off as well, then this new partnership with Firefox may very well be a positive indication of what’s to come for Yahoo.

Valuation: Yahoo’s situation after Alibaba’s fruitful IPO

Yahoo still holds a 15% stake in Alibaba (approximately 383 million shares) and at the going price of $113.28, the value of these shares alone stand at $43 billion ($28 billion after taxes) whereas Yahoo’s current market cap is approximately $50 billion. If you also take into account Yahoo’s 35% stake in Yahoo Japan, which is worth approximately $5 billion after taxes, then Yahoo’s stake in both Alibaba and Yahoo Japan amount to about $33 billion if after taxes. If you also take into account the $8.3 billion (taxes have been deferred for a year) that Yahoo just received from its recent sale of Alibaba shares and a net cash holding of $1.5 billion, Yahoo is sitting on about $42.8 billion in holdings not related to its core business. Subtract that from Yahoo’s current market cap of $50.6 billion and you get a core business value of about $7.8 billion dollars. Yahoo has a billion shares outstanding, so Yahoo’s core business is valued at about $7.80 a share. The value has appreciated significantly since Alibaba’s IPO 2 months ago where investors valued Yahoo’s core business at almost nothing. Yahoo’s core business generates $4.62 billion in revenue in year, with approximately $772 million EBITDA.

The current question is whether or not Yahoo’s core business is worth $7.80/share.

Let’s take a look at Yahoo and some of its main competitors:

Even though their market caps are relatively different, I used the market comparable rule in this case, which states that companies only have to fall within 1/5 of the comparable company’s market cap. Google is one of Yahoo’s biggest competitors when it comes to advertising, but at the same time, has almost 7 times the market cap, so I felt it was better not to include it in this comparison. As for AOL, it has been a long term competitor of Yahoo, being around since the dotcom age, so I thought it might be an interesting point of comparison. Facebook and Twitter are both social media websites and among the main competitors who fight against Yahoo for advertising revenue.

Moving underway, let’s look at some valuation metrics:

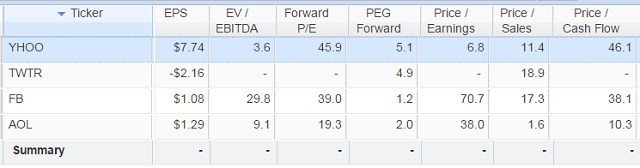

The first thing to notice should be Yahoo’s extremely high EPS in comparison to its peers, which is in fact skewed due to the influx of cash it recently received from Alibaba’s IPO. During the year before this, Yahoo’s EPS was $1.30, which is comparable to both Facebook and AOL. Yahoo’s EV/EBITDA is much lower than its peers and a low EV/EBITDA value may indicate an undervalued company, but this number is misleading in the same way that its EPS is, as it is also elevated because of its recent cash inflow from Alibaba (shown below). P/E was also included for context as it further demonstrates that investors don’t believe in Yahoo’s future earning potential.

Switching to forward P/E, Yahoo’s is significantly higher than its current P/E suggesting that earnings will not grow. Contrarily, both Facebook’s and AOL’s forward P/E is half their current P/E, which is desirable as that means earnings are expected to grow in the future. Another metric that further supports the idea of Yahoo’s diminishing revenue growth is its PEG forward. Yahoo has the highest PEG forward out of the four, which is not good news for Yahoo as that means it is not undervalued from an expected future earnings perspective.

Taking a look at Price/Sales, it can be seen that Yahoo is in between Facebook, Twitter and AOL, which is neither a good or bad thing. A lower ratio may indicate possible undervaluation while a ratio that is significantly above the average may suggest overvaluation. The Price/ Cash Flow of Yahoo is extremely high and may indicate overvaluation because Yahoo is an established company with stable cash flow, but has experienced a huge spike recently because it has been in the headlines due to its position with Alibaba. Therefore, its growth prospects are comparably different from before and may also be inflated due to investor speculation and having a positive cognition from being associated with Alibaba. Facebook is in the same boat regarding expectations for growth prospects whereas AOL is on the opposite end of the spectrum. It, like Yahoo, is an established company, and can be considered a utility with stable cash flow and few growth prospects, therefore trading at a lower valuation. To me, this is why it is curious that Yahoo’s Price/ Cash Flow is trading at such a higher valuation, even after taking into consideration Alibaba’s IPO.

Profitability:

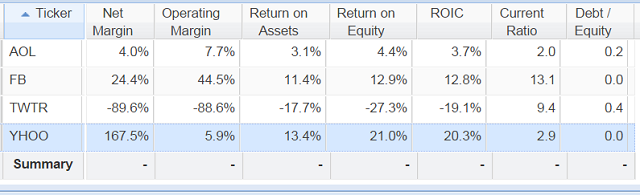

Yahoo is a large company with most of its value attributed to its assets, but is still a profitable company nevertheless as demonstrated by its operating margin, ROA, ROE and ROIC ratios (shown below). Let’s take a look at some of the profitability ratios that dictate Yahoo’s share price and earnings in contrast to its competitors.

Some of Yahoo’s ratios are skewed due to its recent influx of cash from Alibaba, but regardless of which, judging from past performance, its profitability ratios are still very positively strong (shown below).

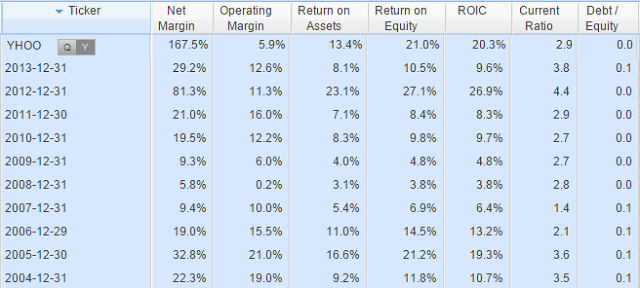

Yahoo’s net margin has had its ups and downs, but the general consensus is still that Yahoo is a profitable company, as further demonstrated by its operating margin. Yahoo’s ROA, ROE, and ROIC are all above its competitors and has never been negative in the past 10 years. Another good indicator of Yahoo’s financial condition is its current ratio, which has stayed above 2 consistently for the past 6 years. Lastly, Yahoo has used almost no debt whatsoever to fund its operations and multiple acquisitions in the past 10 years, which is good sign that Yahoo is able to sufficiently sustain itself without the use of debt.

As for Twitter in all of this, it just means that Twitter has not yet turned a profit and there’s no guarantee that it will do so in the future either: “We have incurred significant operating losses in the past,” the company said, “and we may not be able to achieve or subsequently maintain profitability.” On the other hand, Twitter is a growing company that is investing and rapidly expanding through both acquisitions and operations growth. Twitter is still a wildcard at this point while its competitor Yahoo has produced safer results in the past.

Income Statement

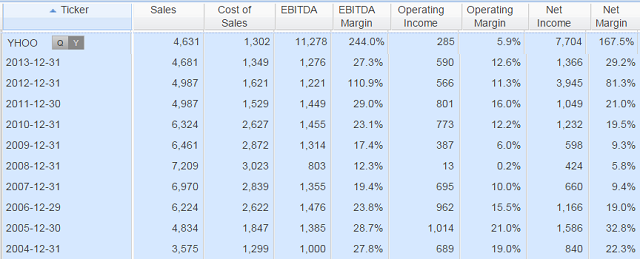

Let’s see how Yahoo’s income statement has changed over the last 10 years:

One of the reasons why I worry Yahoo is a declining business is because its sales have dropped almost yearly since 2008 and are expected to reach only $4.35 billion this year. On the other hand, Yahoo has still managed to generate positive net income for 10 years and also has good earnings stability, being able to generate positive earnings for 10 years straight. These positively reflect on Yahoo’s core business. Even though net margin and operating margin are not steady, they have still been reliably positive showing the relative stability of Yahoo over the years.

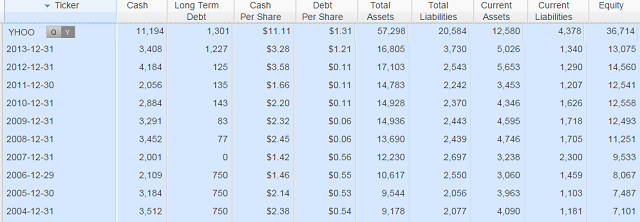

Balance Sheet

Yahoo’s financial health, as seen from its balance sheet (above), is in fact very healthy. Over the past 10 years, Yahoo has had a very stable pool of cash on hand while at the same time maintaining almost no debt in comparison.

Conclusion

Yahoo has had declining sales since 2008 and has been increasingly threatened by the rapid growth of Google and the appearance of Facebook—both have taken a chunk of Yahoo’s ad-based revenue. CEO Marissa Mayer is doing a lot to change Yahoo and is trying to steer it in a better direction, but so far, results have been less than satisfactory. However, if Mayer’s strategy begins to work and results show, then Yahoo will appreciate strongly. Likewise, Yahoo recently showed strong Q3 results and if it continues at this rate, then I see no downside in investing a small amount, even more so if Yahoo is able to make some good acquisitions (AOL) and is able to take big steps in the marketplace such as its recent partnership with Mozilla Firefox.

If you expect Alibaba to continue to do well, then Yahoo should also subsequently perform well. Yahoo has already appreciated significantly recently, jumping from the $40 range to $52 currently, meaning that Yahoo has, for the most part, appreciated to an appropriate value that investors deem reasonable for its current standing. The best time to buy into Yahoo for big gains may have already passed as the stock seems to have reached its current true value. But it is still may not be a bad idea to invest in Yahoo going forward. Its assets and cash are a good hedge against downside risk. If Alibaba continues to do well and if Marissa Mayer’s acquisition strategy starts to perform in 2015 as she expects, there could be still more appreciation on the horizon.

Top