Alibaba: Is the price justified?

Printer Friendly

Printer Friendly

It’s no doubt that for the six weeks investors have had their eyes on the e-commerce sensation Alibaba (BABA), who had the biggest U.S.-listed IPO in history, being valued at an astounding amount of $167.6 billion during its opening day on September 19. That’s more than double eBay’s (EBAY) $64 billion market value and it even tops the market cap of Amazon (AMZN). Surprisingly, Alibaba is the fourth most valuable technology company in the world, beating out IBM, Samsung and even Facebook.

Despite its size and market value, Alibaba represents uncharted territory for many U.S. investors because of its foreign origin as well as the lack of historical public financials for investors to examine. However, that hasn’t deterred Alibaba’s stock price from rapidly rising. Initially priced at $68/share when it opened on September 19, Alibaba quickly jumped to an opening trade price $92.70/share and closed at $93.89 on the same day, a 38% increase from its initial price.

There are still a lot of mixed opinions about Alibaba’s overall value—is it a fad stock or is it a genuine winner? Because I was also extremely curious about Alibaba’s pricing, I decided to take a closer look at the company’s overall structure, prospect for growth, and financials to determine if it could be a worthy investment for risk-averse investors like myself or if it’s just cowboy territory now.

First things first: What is Alibaba and how does it make money?

Alibaba is a gigantic e-commerce company that operates online marketplaces for both international and domestic China trade. It is the world’s largest online and mobile commerce company by gross merchandise volume — Alibaba’s gross merchandise volume of $296 billion surpasses the combined value of both eBay ($88 billion) and Amazon ($116 billion). It provides mainly consumer-to-consumer and business-to-consumer sales services through web portals that are also some of China’s most popular online shopping areas, including Taobao (C2C), Tmall (B2C), and Juhuasuan (group buying). These three marketplaces alone generated a combined gross merchandise volume of CNY 1.833 trillion (USD 296 billion) in the twelve months ended June 30, 2014. Furthermore, Alibaba’s China retail marketplaces consist of 279 million active buyers, which is more than 20% of the Chinese population. Alibaba also offers electronic payment services through its third-party online payment platform, Alipay as well as a shopping search engine, eTao that acts as a comparison shopping website.

Surprisingly, the majority of Alibaba’s revenue does not come from the transaction fee associated with connecting buyers and sellers, but actually from advertisements. Alibaba uses the widespread popularity of its online platforms to its utmost through advertisements. The way advertising works on Alibaba’s websites, mainly Taobao and Tmall, is very similar to Google’s (GOOG) AdWords, which are search-linked ads: Merchants on Alibaba’s platforms participate in auctions of search keywords and the highest ranked item is from the merchant who placed the highest bid and is willing to pay the most per click of the product. Alibaba also charge for other ad spaces on their homepage. Taobao’s ad revenue through March was about $1.24 billion – more than half of Alibaba’s $1.96 billion revenue. The other half comes from Alibaba’s B2B business and other business revenue including commission collection.

Alibaba now controls 84% of all online sales in China, which more or less means it dominates the Chinese e-commerce marketplace. A growing trend in recent years has been the robust growth of online shopping, especially in China, where competition from brick-and-mortar retailers is minimal. Alibaba is poised to benefit from this trend as currently over 80% of all online shoppers use Alibaba, so the continued relevance of Alibaba in China’s online marketplace can be reasonably expected for many years to come. However, there will without a doubt be new competitors like Tencent and Baidu rising up to challenge Alibaba.

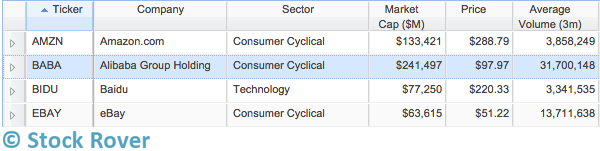

Alibaba managed to establish a central presence in China and since it will get increasingly harder for Alibaba to take control of the remaining market share in China, Alibaba will probably shift its focus towards oversea markets, specifically looking to gain a foothold in places like the U.S. and Europe. With this in mind and the fact that founder Jack Ma explicitly said himself that Alibaba was looking to expand globally, I compared Alibaba against Baidu (BIDU), potentially its largest Chinese competitor, and its U.S. competitors, eBay (EBAY) and Amazon (AMZN). Here is a table comparing market cap, price, and trading volumes for the four companies:

While these companies range a bit in size and trading volume, you can see that they are all big dogs. Another thing to keep in mind is that Alibaba’s market cap of $241 billion is much larger than Amazon’s and eBay’s combined market cap of ~$196 billion even though Alibaba’s IPO was only roughly a month ago whereas Amazon had a five year head start on it. Is this an indicator of Alibaba’s overbearing footprint as it steps into the market or is it just an overblown number caused by investor speculation?

Corporate Structure: What am I Actually Buying?

Something to take into account when looking at Alibaba is the company’s corporate structure (shown below), which is not only complicated, but risky for U.S. investors. Alibaba is using a structure known as the variable-interest entity, a method used by other Chinese tech companies that list in the U.S. such as Baidu. When an investor buys shares in Alibaba, he isn’t really buying shares in Alibaba, but is actually purchasing a stake in a registered entity in the Cayman Islands that is under contract to receive the profit from Alibaba’s Chinese assets without actually owning them.

Essentially what this means is that the key assets of Alibaba will be controlled by Jack Ma, co-founder and executive chairman of Alibaba, and another founder, Simon Xie. The companies that hold major stakes in Alibaba include Yahoo (16.3% ownership) and Softbank (32.4% ownership), the Japanese tech firm that owns Sprint, have relatively little to no power in the operational activities of Alibaba—they surrendered their shareholder influence to a group of executives called the Alibaba Partnership, which includes longtime Alibaba employees such as Jack Ma and his right-hand advisor Joe Tsai. Alibaba also has a board of directors, but the Alibaba Partnership reserves the right to nominate the majority of the board members, meaning the Partnership controls the activities and decisions of the company by default without the need for input from other shareholders. Jack Ma and his group of executives have almost full dictatorship of the company and is not required to act in the best interest of Alibaba’s shareholders, so there is a lot of inherent risk for investors that comes from the corporate structure alone.

Furthermore, problems concerning Alibaba’s management have arisen before. The ability of Alibaba’s executives to act independently allowed Jack Ma to spin off Alibaba’s previously fast-growing payments platform, Alipay, to another company that he owns in 2011, which greatly angered Yahoo. (I’ll be looking more closely at Alibaba’s implications for Yahoo in my next article.

Jack Ma: Champion or Trickster?

Jack Ma’s story started at the tender age of 12 where he started guiding foreign tourists around the city in an effort to improve his proficiency of the English language. Years later, Ma went on to graduate from Hanzhou Normal University in 1988 with a bachelor’s degree in English, which eventually led to Ma becoming a teacher who taught English at a local college, but not before being rejected for positions at a local KFC, a hotel and the city police. Ma set up his own translation company and had his eyes opened while on a business trip to the United States in 1995: he noticed the enormous potential of the Internet market and used his opportunity to start his dream by working in Beijing for an internet firm under the Ministry of Commerce where he then proceeded to create Alibaba in 1999.

From $60,000 to China’s richest man is how the story goes, but the question at large is whether or not Jack Ma will treat investors well. For growing technology companies like Facebook, Twitter, and Alibaba, people aren’t buying a stake in the company, but are essentially betting on Mark Zuckerberg, Jack Dorsey, and Jack Ma as well as their future plans for the company. Ma managed to achieve greatness from nothingness, but he has since cashed out on his winnings, stepping down from his CEO position and instead choosing to focus on philanthropy. However, Ma still retains the role of being Alibaba’s backseat driver because he will still shape the company’s strategy and maintain the title of executive chairman.

Jack Ma has tremendous ambition and is extremely driven, but at the same time, may be too focused on his ideal goal, which remains all but unknown to investors except for Ma’s intentions to penetrate the western markets. Ma definitely has a vision and end-goal for Alibaba, but his decisions when dealing with Yahoo and Alipay’s split from Alibaba may suggest that his interests might not align with the shareholders’ and that his ultimate goal lies elsewhere, in a place without concern for his shareholders.

Where is Alibaba headed?

Alibaba’s growth has been overwhelmingly successful in the past couple years. The question though is whether or not this growth is sustainable — Alibaba relies mainly on advertisement revenue as well as its strong market position to maintain its current growth. Its EPS this year grew at an astounding rate of 181% and is expected to average a 26.83% EPS growth rate over the next five years (shown below), so it can be certainly argued that the company has good future prospects.

(Alibaba’s EPS)

As a whole, its profitability ratios also support this analysis as its ROE stands at 86.4% and its ROA and ROIC at 30.8% and 41.4%, respectively (all shown in the table below). These ratios indicate that Alibaba’s current financial health is very strong. In comparison to both Amazon (whose strategy involves razor-thin margins) and eBay (whose margins have taken a significant hit due to higher operating expenses as the company increases spending on sales, marketing & product development), there is an obvious winner with Alibaba leaving both competitors in its dust trail. Furthermore, as shown in the table, Alibaba’s net margin and operating margin blow its competitors out of the water, reaffirming Alibaba’s future prospects for growth. Baidu, on the other hand has very solid margins and strong profitability ratios meaning that it could potentially give Alibaba a run for its money if it decides to join the e-commerce market.

Next, I took a look at the companies’ current ratio (second to right-most column above) to see if Alibaba and its competitors have enough cash on hand to adequately pay off their short-term obligations. In the cases of the three online retailers (Amazon, eBay & Alibaba), none had a current ratio of 2.0 or greater, which is usually the case when it comes to retailers – high-end retailers are able to negotiate long credit periods with their suppliers, which explains why they have high trade payables. Conversely, retailers are extremely stingy when it comes to offering credit to customers, so they will generally have lower trade receivables. However, unlike Amazon and eBay, Alibaba merely acts as a third party liaison and does not carry any inventory whatsoever, so there is a cause for concern here since Alibaba may have trouble coming up with cash when the time comes.

I then looked Alibaba’s debt/equity ratio, which is 1.1, indicating that Alibaba has been aggressive in financing its growth with debt and this can result in volatile earnings as a result of the additional interest expense. In comparison to Amazon, Baidu and eBay, Alibaba has higher than normal debt/equity and is in a riskier position should earnings fall short of expectations.

Long story short, Alibaba’s endeavors take on more risk in comparison to its western competitors, Amazon and eBay, but its returns have been absurdly high, so the risk appears to not be a bad choice if things go as planned. On the other hand, if growth and returns fall, then Alibaba could be in a drastic situation and the share price may in turn respond by plummeting.

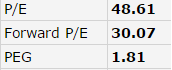

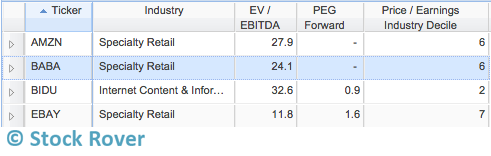

I wanted to also look at some valuation metrics for some context, as high-growth stocks can sometimes be driven by investor sentiment rather than actual performance. I looked at EV/EBITDA, PEG Forward, Price/Earnings and industry decile as a comparison against the industry as a whole (shown below).

(Alibaba’s metrics)

Alibaba’s current P/E of 48.61 and forward P/E of 30.07 suggests that the company may be overvalued or that investors are expecting a lot of growth from this company. Since Alibaba has just debuted, the latter seems to be the case. The EV/EBITDA of Alibaba is acceptable as its value is similar to Amazon’s.

Shifting our focus from Alibaba to eBay for just a moment, take note of eBay’s comparably lower EV/EBITDA — a low EV/EBITDA indicates that a company may be undervalued and is also often used to find attractive takeover candidates — I bring this up because there has been speculation that Alibaba is looking to acquire eBay. EV/EBITDA is a good valuation metric to use when it comes to acquisitions because it takes into account the amount of debt the acquirer will have to assume, which attaches a more realistic number value to the company being acquired. Generally, companies with low EV/EBITDA values are regarded as potential takeover candidates and since eBay’s EV/EBITDA value is considerably lower than Alibaba’s, there may be some truth in that speculation.

Another side note to take into account is that eBay recently announced that it will split PayPal and eBay into two companies, effectively halving eBay’s $64 billion market cap, which calls for further suspicion. As thisSeeking Alpha article argues, Alibaba has significant reason to acquire eBay as not only do both companies operate in the same industry, but eBay’s financials have no underlying problem, so both eBay and Alibaba would benefit from this acquisition.

Alibaba’s high PEG forward of 1.75, however, may be an indicator that Alibaba may be overvalued and, when compared to both Baidu and eBay, the ratio is still higher. The PEG ratio is generally considered to provide a more complete picture as it takes into account the company’s earnings growth. A general rule of thumb is that a PEG of under 1 is desirable and the lower the PEG ratio, the more the stock may be undervalued given its earnings performance. I also included P/E industry decile to generate a better understanding of the company’s value. A lower decile score indicates better performance relative to the industry and in this case, Alibaba outperforms both Amazon and eBay, but is not comparable to Baidu as they are in different industries.

Alibaba’s currents earnings are off the charts and its future earnings growth also seems to be poised for success, but the PEG ratio is telling us that the current stock price may be more bark than bite. The conventional wisdom is that one should wait for at least 90 days after a company’s IPO before investing into the company, as usually the hype will have died out by then – some examples of where this wisdom would have played out well include Facebook and Vonage.

Alibaba’s success in China may not reciprocate the same results in western markets unless Jack Ma has a clear map for success – Ma saw a clear business opportunity with the online retail market in China and took it, acting before any of his competitors could respond, allowing Alibaba to enjoy a first mover advantage and establishing a strong user base foothold in the Chinese markets. This advantage was key to Alibaba’s success as its massive user base generated more newcomers which led to more trust and veracity as well as higher retention rates of users, serving as a barrier to entry for competitors like eBay. Furthermore, knowing the right people in the right places is what makes all the difference, especially for Jack Ma and a growing economy like China—Alibaba benefited greatly by being on friendly terms with the Chinese government, contributing momentously to the company’s widespread success.

Alibaba will not be enjoying the same benefits it received in China—rather, there will be significant opposition from already established companies like Amazon and eBay.

Conclusion

Alibaba is without a doubt right now a very strong company. However it is clear that value investors should steer clear. While Alibaba’s valuation metrics are high, they are not unprecedented for technology companies, but there is still an inherent risk due to Alibaba’s risky management structure, lack of historical financial data, and potentially lackluster results in western markets where competition is greater. However, I give more risk-tolerant investors the green light on Alibaba, as the expected returns outweigh some of the potential risks associated with this investment. This is a major growth opportunity for growth investors because if Alibaba continues to grow at its previous rate, then its returns are bound to be astronomical. Likewise, if an investor is willing to bet on Jack Ma’s brilliance and believes that Ma can continue to rake in high returns, then Alibaba is a worthwhile investment opportunity.

I personally am a very risk-averse person, so I like to research, investigate, wait, wait, analyze and then wait some more before deciding whether or not I want to invest in something. While I am interested in Alibaba as a company and keen to see where it goes, I will do so from the sidelines for now. I may invest later when I feel assured that Alibaba is on solid ground and its valuation is not sky-high.

Top