Quality at a Reasonable Price

Printer Friendly

Printer Friendly

For several years the price/earnings ratio of the S&P 500 has been steadily creeping further into a rarefied zone, and we fear the stock market is in a precarious place of overvaluation. This means that good deals are hard to come by. We took this as a challenge and set out to find a few good stocks that are reasonably priced.

Download our Quality at a Reasonable Price watchlist for free from our library so you can run these selections through your own tests. Just go to ‘Browse Library’ in the Start menu and navigate to the watchlists section from the lefthand menu. Here it is:

We found these 9 stocks by skimming the results from multiple screeners in Stock Rover—screeners focusing on growth, profitability, value, or some combination of those. All are over $8B in market cap because we were interested to see which larger, well-known companies were affordable right now.

Before getting into what we like about these stocks, please note that this watchlist represents a first pass of research only; we have not done a deep dive. Follow up with your own research and keep an eye out for a future article on our blog in which we dig deeper into one of these picks.

Value

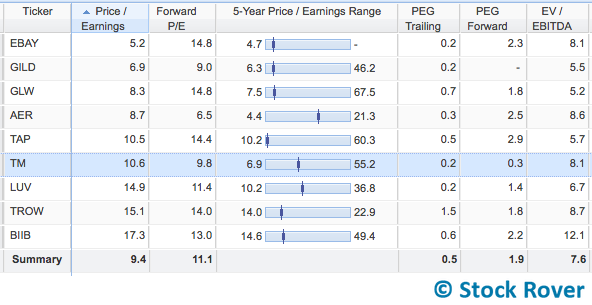

First let’s take a look at why all of these picks look to be good or reasonable values. The table below (in the ‘Valuation’ view tab) shows how each is inexpensive either relative to its historical price/earnings (P/E) or relative to its expected earnings growth (or both).

Ebay (EBAY) is the cheapest by this classic valuation metric, with Gilead Sciences (GILD) close behind. Meanwhile, T. Rowe Price Group (TROW) and Biogen (BIIB) have valuations that are almost three times higher. However, they are still well below average—for the S&P 500, the average P/E is above 25 right now and the median P/E is about 22. It would also be worth comparing each stock’s P/E to their industry averages (found in the Valuation section of the Summary tab of the Insight panel).

As you can see in the center column, all of these stocks are well below their historical 5-year P/E high, and many are at the very low end of the range. This means that, regardless of the market’s valuation, each of these stocks is comparatively inexpensive given its own historical valuation.

Forward P/E compares the current price to an estimate of earnings for the next fiscal year. About half of the group has a forward P/E that is lower than the current P/E, meaning that earnings per share (EPS) is expected to grow in the next year. Additionally, all of the forward P/Es are below the S&P 500 median of 17.2.

(By the way, you can see the S&P 500 median for almost any metric by right-clicking that column’s header and selecting ‘Explain’ from the menu. This opens a handy box with the metric definition and benchmark values, as well as links to related metrics. Try it out!)

All but TROW look to be undervalued according to either or both of the PEG trailing and PEG forward metrics, which compare the P/E against the past 5 years of growth or expected 5 years of growth. Take the PEGs with a grain of salt, but they still serve to provide context for the P/E value.

Finally, EV/EBITDA further makes the value case. This metric compares the market’s value of the business (enterprise value) to its earnings before interest, taxes, debt, and amortization (EBITDA), which evens the accounting playing field so that companies with different capital structures can be compared. All of these companies have EV/EBITDA below the S&P 500 median of 13.1 and a handful are close to or below its 10th percentile value of 6.6.

Quality

Of course, an inexpensive valuation doesn’t necessarily mean a stock is a good value (it could be cheap because it’s terrible!). So let us make the case for why these stocks aren’t terrible.

“Quality” is subjective, but a common way of determining quality is by looking at a company’s profitability. In the table below we see that all of these companies have positive return on equity (ROE), assets (ROA), and invested capital (ROIC), and all but Toyota (TM) have margins in the double digits. (Learn more details about all the metrics below in our profitability metrics explainer.)

The ‘Rank Within Table’ column shows the 9 stocks ranked by a profitability screener which includes all the metrics above as well as a few comparing profitability versus industry.

Although not shown in the table, we also took a look at profitability history (you can open historical data in the table by clicking the carrot at the far left of any row—see here for a screenshot). Some, such as Molson Coors (TAP) show a trend of improving profitability over time in most metrics; others have mixed trends, but all have a record of positive returns and margins.

For further context, compare each company’s profitability against others in its industry. You can easily do so by adding any of these metrics to the Peers tab of the Insight panel.

Growth

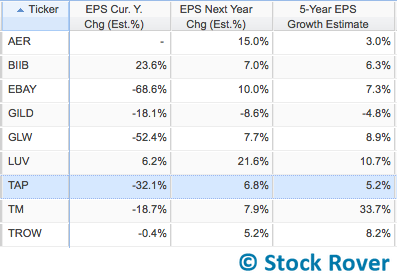

A survey of EPS, sales, and operating income growth gives us mixed results. Many of these companies have had negative growth in the last year, but strong growth over the 3- and 5-year periods. Others, like TAP and EBAY, had such banner years that earnings for the coming year are expected to come down.

Here’s the table. We’ve color-coded the growth columns for EPS, Sales, and Operating Income so it’s easier to see each category. (To color columns in your own tables, right-click a column header for the option to add color; you can also color rows by right-clicking.)

And here are the expected EPS changes for this year, next year, and the next 5 years. While many are negative for the current year, most are expected to see earnings growth beyond this year.

GILD is the outlier. It’s the only company to have negative numbers in the next year and 5-year estimates. In fact, GILD is probably one of the chancier picks on this list (more on that later).

Dividends

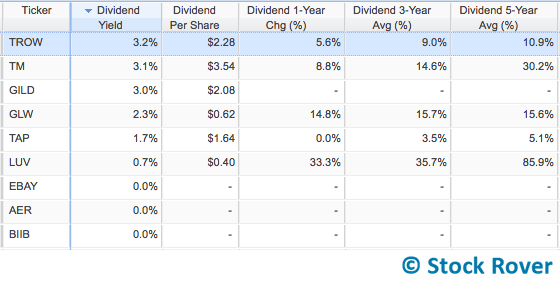

A few of these might be interesting to the dividend fans among you. None of these were selected from dividends screeners, but several do pay dividends. Here they all are sorted by yield, with dividend growth over 1-, 3-, and 5-year periods shown as well.

TROW, TM, and Corning (GLW) all provide modest dividends that have been increasing over time. Southwest Airlines (LUV) has a low yield but also has dividend growth. GILD just started paying a dividend in 2015 and is already up to a respectable yield, although we don’t have enough history to know how committed the company is to maintaining or growing its dividend.

Final Notes

Based on the numbers above, these companies are solidly profitable and offer modest growth expectations, and all are available at a nice price. To us, this means they warrant further investigation as potential long-term investments.

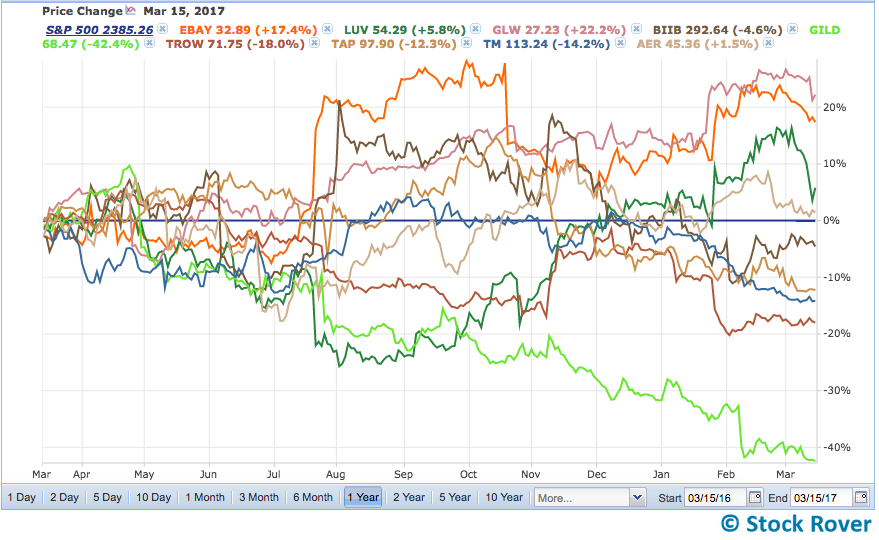

What about Gilead? This one stands out for its negative growth expectations, and also for its abominable performance in the last year. Take a look at all the stocks charted against the S&P 500 (set as a baseline). GILD is easy to spot as the plummeting lime green line:

Of course this performance is part of why the stock is so alluringly cheap right now. Then again, GILD has been alluringly cheap before, too (such as one year ago). However, biotech is turning bullish and GILD is currently being pressured by investors to make an acquisition (specifically, Incyte (INCY)), or to at least “do something.” In short, we kept it in this list because we think it is an interesting time for the company with the potential for upside.

More qualitative research is needed for all of these companies to determine if they have good strategy and management (see our CEO’s article on how to evaluate management). It’s worth noting that all the picks have an average analyst rating of “Buy,” except GLW, which has a “Hold” rating, and AER, which has a “Strong Buy” rating.

Are you one step ahead of us? Chime in with your insights!

Comments

Comments are closed.

Top

I am happy with this screening “first cut” that you have presented. I am distilling it further ; probably to a top 3 or top 5 to refresh my opportunity list.

Thank you.