AerCap: Feeling the Tailwinds

Printer Friendly

Printer Friendly

Last month, we published a list of 9 stocks that looked to be reasonably priced in the current expensive (some might say overvalued) market environment. In this article, we drill down on the smallest and least well-known of the bunch, AerCap Holdings (AER), which has a market cap around $8 billion.

AER is the only one of the watchlist 9 that averaged a “Strong Buy” rating from analysts (most of the others were rated “buy”). Since we at Stock Rover always like to explore under-the-radar picks, we wanted to learn more about this company to see if we agree with the analysts’ rating.

About AerCap

AerCap is an aircraft leasing company headquartered in Dublin, Ireland and has been publicly traded on the NYSE since 2006. They make money leasing aircraft and engines to airline companies, as well as selling assets—usually older aircraft or aircraft parts.

As of the end of 2016, the company had 1,566 aircraft in its portfolio (owned, managed, or on order), making it the world’s largest independent aircraft leasing company and one of only a few global aircraft lessors. It has a diversified revenue base, with approximately 200 customers in about 80 countries and the top 5 lessees collectively accounting for only 23% of total lease revenue. AerCap has grown both organically through business expansion and inorganically through acquisitions.

Dividend diehards can turn back now. AerCap does not pay a dividend.

Growth

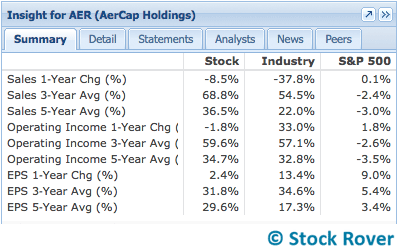

AER has outpaced its industry in the last 5 years in sales, operating income, and earnings growth. Take a look:

AER’s strong 5- and 3-year averages are in large part the result of the acquisition of International Lease Finance Corp, which was completed in May 2014 and caused revenue to more than double, plus increase another 45+% in 2015. Such a spike accounts for the negative 1-year change in sales.

Future Growth

In its investor relations materials and on the most recent earnings call, AerCap stresses its strong position with regard to growth. A key factor is the growing global demand for air travel. The International Air Transport Association (IATA) predicts traffic growth of 5.1% in 2017 (which is down from 2016’s 5.9%). However, it also notes that “capacity growth will outstrip the increase in demand, thus lowering the global passenger load factor to 79.8% (from 80.2% in 2016),” but this lower load factor will be “offset somewhat” by an anticipated 2.5% increase in world GDP.

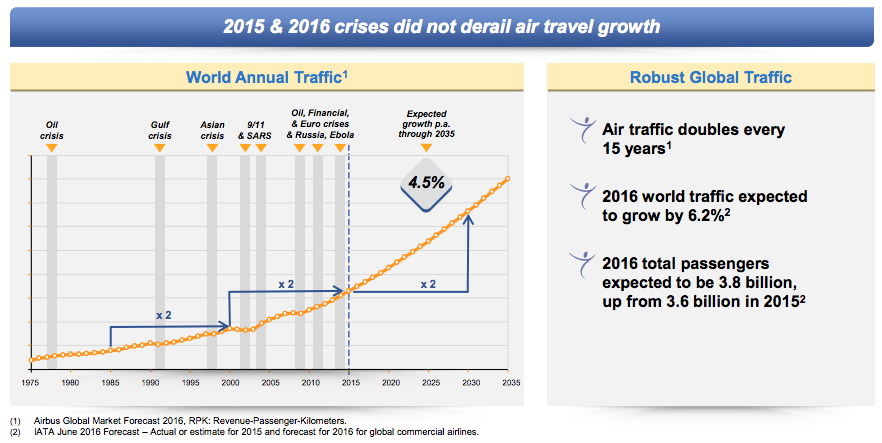

Even with the anticipated growth in global GDP, there are worrisome global trends. AerCap acknowledges that the seemingly nonstop stream of large-scale crises worldwide (from Ebola to Brexit to terrorist attacks) may make it seem like “the sky is falling,” but they insist that, at least for the air travel industry, it is not. The resilience of air travel can be seen in the following slide from the company’s 2016 Investor Day presentation. The graph on the left shows how the growth of air travel persisted through a variety of political, economic, and health crises.

2016 AerCap Investor Day Presentation

2016 AerCap Investor Day Presentation

The company also points to an Airbus market forecast saying that air traffic doubles approximately every 15 years and is projected to more than double from 2016 to 2035. Naturally, this air traffic growth directly benefits lessors like AerCap because “robust traffic growth continues to fuel demand for additional aircraft.” (2016 20-F)

Furthermore, the financing environment appears favorable toward airline expansion. From CEO Aengus Kelly in the most recent earnings call: “Looking ahead to 2017, we expect to see stable levels of growth in the market and this will be supported by the 8th year in a row of aggregate airline profitability. Our airline client also remain well supported by favorable financing environment, with the debt and capital markets looking to participate in the need to finance growth in the sector.”

Profitability

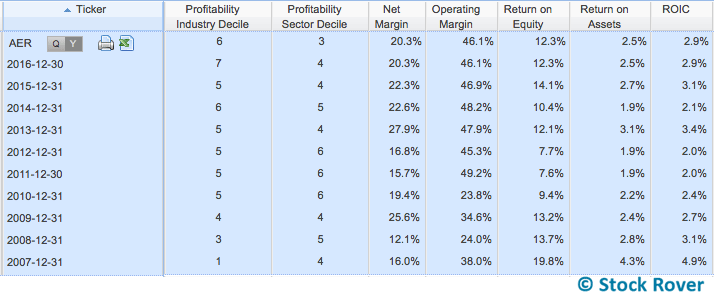

In addition to benefitting from increased industry-wide demand, AER’s position as the largest aircraft lessor and the scalability of its business model (which is discussed at length in this excellent article) give it a platform to further increase its profitability. A smart, competent management team is needed to make the most of those advantages. There is evidence to suggest that AerCap is well managed, including a 99.5% fleet utilization rate last year and good performance in profitability metrics (seen below).

The following table shows AER’s profitability and profitability over time. Its current net margin and operating margin are both more than double the industry averages. Its ROE, ROA, and ROIC are all fine, although they are middling or below average when compared with peers. Most metrics have come up significantly since 2010/2011. Before that, the company’s profitability was apparently in decline since 2007.

Note that AER’s current CEO Aengus Kelly has been at the helm since 2011, having worked in the air finance and leasing business since 1998 and as an executive at AerCap since 2008. The generally rising profitability trends since his transition to CEO can provide a measure of confidence in his leadership.

Another interesting thing to note about the above table. While the profitability sector decile column shows that AER’s profitability relative to its sector has moved from the top 60% to the top 30% (a strong improvement), the profitability industry decile is less decisive. AER’s profitability score has been wavering somewhere in the lower half of its industry for years. This is a sign of how the Airports & Air Service industry as a whole has become more profitable relative to the Industrials sector.

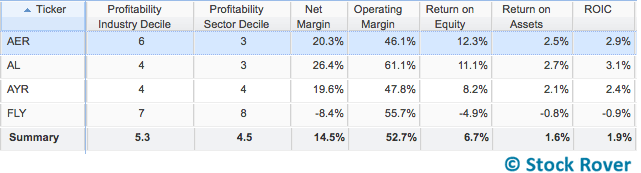

Here is a profitability comparison to some of AER’s direct competitors, aircraft leasing companies:

AER compares favorably to its peers, but it’s not a slam dunk. Air Lease (AL) beats AER in all but ROE. Although this does not diminish AER’s performance, it does pique our interest in AL, which incidentally is also rated a “strong buy” by analysts. One of the benefits of doing peer comparison like this is that it can introduce you to yet more under-the-radar picks. But that is research for another day. Back to AER.

Debt

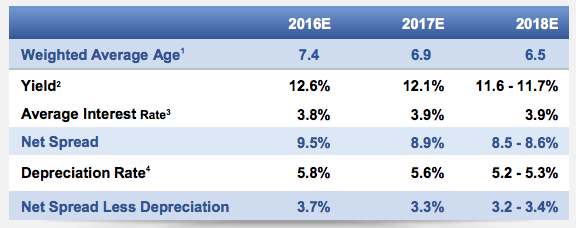

Because of the capital-intensive nature of its business, AER maintains a high level of debt. This does not necessarily point to a problem with financial health. Like a bank, AER benefits from the spread between what it pays to finance its fleet and the yield from its lease rents. The following slide illustrates how the company estimates it will earn a net spread (less depreciation) between 3.2 – 3.4% in the next two years:

2016 AerCap Investor Day Presentation

2016 AerCap Investor Day Presentation

Of course, high leverage entails inherent risks, which are enumerated in detail starting on page 8 of the 20-F. One key risk is the high cost of debt service (interest payments), which absorbs a significant portion of the company’s cash flow. Another risk is sensitivity to the cost of borrowing; if interest rates go up or the cost of borrowing increases, it could directly affect AER’s bottom line. However, on the Q4 earnings call Kelly provided some comfort vis-à-vis rising rates, pointing out that AerCap runs a “hedged book” and “any lease that’s placed on forward order has an automatic adjustment for any increase in interest rates.” He added that rising rates tend to correlate with a better global growth environment, creating “asset insulation.”

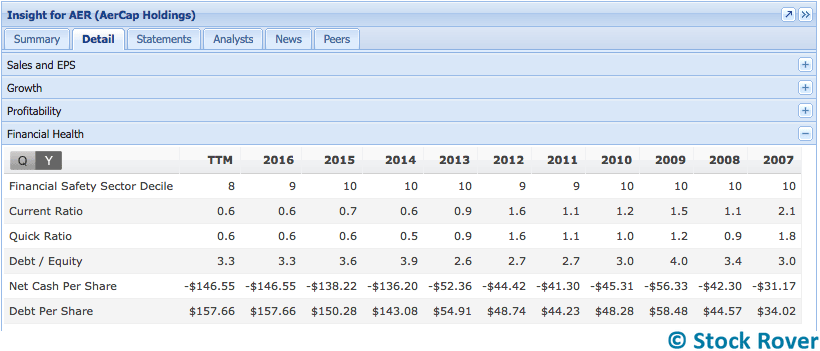

Below you’ll see AER’s financial health numbers over time, starting with trailing 12 months in the leftmost column. Debt has increased steadily over time (debt per share), while debt/equity (D/E) has bobbed up and down, and the overall financial safety sector decile has mildly improved.

The stated target D/E range for the company is between 2.7 and 3, and they reported an adjusted D/E of 2.7 in Q4. That reported value is quite a bit lower than the GAAP value of 3.3 shown in Stock Rover, but it at least means that they are, by their own measure, hitting their D/E goal.

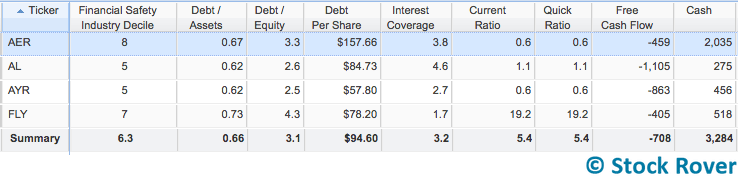

Below we compare AER to peers in these and other measures of financial safety.

AER has comparable or less financial safety than its peers, but not necessarily to a worrisome degree. Once again, AL is looking strong among its peers.

One important vote of confidence in AER’s health is Moody’s recent upgrade to investment-grade Baa3. Moody’s cites AerCap’s improving fleet risk profile, strong liquidity, and operational stability among the reasons for the upgrade.

Valuation

We originally found AerCap by combing for profitable companies that were reasonably priced. And with a P/E multiple of 7.8, AerCap’s valuation is certainly undemanding. Next year’s expected earnings growth brings the multiple down further to 6.3. Although this is not the cheapest the stock has ever been, it is well below its 5-year P/E high of 21.3, and on the low end of its more recent P/E range of 7.5 – 9. The price/sales, price/book, and EV/EBITDA values are also on the low side.

Stocks with a good business story usually don’t get much cheaper than this.

Conclusion

As long as you are comfortable with a debt-heavy capital structure and believe the model will continue to perform well in a rising rate environment, we find little to recommend against AerCap holdings. It’s a well-run, geographically-diversified, competitively-positioned company within a growing industry, and shares are attractively priced. It is worth noting that in a number of financial metrics, AerCap is outperformed by a smaller competitor, Air Lease. We think both companies are worth a look—see for yourself if you think they’ll fly.

Comments

Comments are closed.

Top

Excellent report on AER and the leasing industry for airplane services. AER has a lot of pluses and this report surprises some of us by comparing it with a smaller but perhaps more growth oriented due to smaller size and upward price mobility stock Air Lease (AL). Thank you for this information. The leasing business is a arm of and similar to banking in many ways in that long term results depend on the profitability of the borrowers Leasees (airlines) and their ability to repay.

The debt level scares me. I prefer countries and industries that have a better capital balance for safety when things turn rough. Also, not trying to be nit picky but aircraft, as well as the singular, is the plural, not aircrafts.

Companies not countries …………… well, Freudian slip, countries too. LOL

Noted on aircrafts vs aircraft. Article has been patched. I guess aircraft more like sheep and deer than I thought they were.