Intel: Dominant and Undervalued

Printer Friendly

Printer Friendly

Intel (INTC) is the largest publicly traded semiconductor chip maker in the United States, as well as the largest semiconductor company in the world. The microprocessor market accounts for about 20% of the total semiconductor industry’s revenues, and is dominated by two companies, Intel and Advanced Micro Devices (AMD). Intel is the unquestioned leader in the microprocessor market, both in terms of market share and product performance. It ships over 80% of the world’s microprocessors.

Intel has always been a strong company, but recently it has seen a significant increase in share price over the last 12 months, jumping from $23.50 to the share price at the time of writing of $37.43 (shown below). Intel’s share price is up approximately 40% year-to-date in 2014.

Despite some volatility, which you can see in the chart, Intel has overall done outstandingly well in the past year. No one knows whether this performance will continue into the future. However as I discuss in this article, Intel’s past experience, current financials, and expected growth put the company in a pretty good position for continued long term success and stock appreciation.

Revenue Growth

Intel has three main operating segments: PC Client Group, Data Center Group and Other Intel Architecture. The PC Client Group (63% of 2013 sales) makes microprocessors and related chipsets for the notebook, netbook and desktop segment. The Data Center Group (21%) make products such as microprocessors, chipsets and motherboards that are used in servers, storage, workstations and other applications focused around the data center and cloud computing. The Other Intel Architecture Segment and the Software and Services group accounted for the remaining 16% of sales in 2013.

Intel, at the moment, is benefitting from stabilization and share gain within the PC retail market after several years of declining sales, due to factors such as the growth of Apple’s iPads which don’t use Intel microprocessors. The PC market comprises the largest chunk of Intel’s revenue and while there seems to be little to no growth for the overall PC environment in the long run, there is still growth among Intel’s other operating segments. For example, Intel is seeing improved demand in the PC business segment, as businesses are currently in the middle of a PC refresh cycle. Businesses are replacing many of their PCs with upgraded equipment, which is another reason why Intel’s sales have been rising. Likewise, the major revenue source for Intel, sales of PC processors to enterprises and Server Message Blocks, have also been growing.

Intel’s key growth driver in the coming years will be its server processor business, which currently accounts for about one fifth of the firm’s sales. Its Data Center Group is growing at a healthy rate, increasing from an 11% growth in 2012 to a 16% growth this year and is forecasted to continue growing at a 15% rate between 2016 and 2018. Additionally, its growth in Other Intel Architecture Segment will help drive revenues higher. Intel is also rapidly expanding in the mobile device and smartphone and tablet processor market, as demonstrated through its recent announcement of its ATOM processor for the mobile, which should help Intel catch up in terms of power efficiency with ARM-based chips – Intel already has multiyear agreements with Lenovo, Asus and Foxconn to develop mobile devices that run on Intel Chips.

Intel’s revenue heavily depend on its PC Client Group, revenue growth has been impacted by a persistent decline in the PC market as well as increased investment in building out its technologies over the last two years. However, a stabilizing PC market along with Intel’s widening reach in new growth markets has allowed the company to perform better than expected in 2014. The expected growth from its Data Center Group and increased market share in the mobile area should hopefully counteract the declining PC market and in turn generate a healthy boost to Intel’s future revenues.

Intel reported extremely strong Q3 numbers, with $14.6 billion (its largest quarterly revenue in the company’s 46-year history) and increased profits of 12%. Intel’s revenue increased 8% since last year and beat its projected revenue growth of 6% for 2014. Its expected revenue growth for 2015 is 3.9%, according to S&P Capital IQ and is forecasted to be in the mid-single digits, according to Intel. The increased revenue growth seems to have also boosted earnings per share and this in turn has led to increased investor confidence within the stock. The company is making good progress and from my research I don’t see any big road bumps that will get in the way of Intel continuing to grow at a steady pace.

Competition

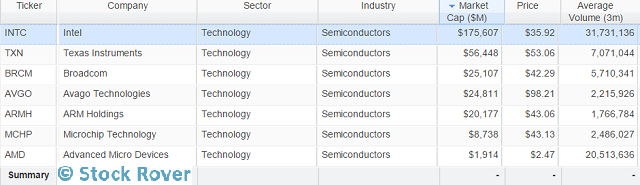

Since Intel deals mainly in semiconductors, I compared the stock against others in the semiconductor industry:

Most of these companies do not fall within the market comparable rule, but as mentioned before, Intel dominates the market by a wide margin, making it difficult to find market comparable competitors. Even though they are much smaller companies, MCHP and AMD are some of Intel’s main competitors when it comes to microchips and semiconductors.

AMD is one of Intel’s main competitors in the x86 PC market (x86 refers to the world’s predominant personal computer CPU architecture and platform, developed originally by Intel but now also found in various AMD brands). However, AMD has been progressively losing PC market share in the last few years and in its current state can be said to be an empty shell, surviving only because Intel would have antitrust issues were it to swallow the company. In return, however, Intel is thriving off the differences in performance between its products and AMD’s, and is capturing extremely high-margins (explained further below). Intel has ‘won’ the PC war, while AMD has shifted its focus onto gaming consoles and other semi-custom chips.

Intel continues to be a dominant player in the semiconductor industry, beating out most of its competitors by a wide margin, but in order to get a more accurate idea of how Intel and its competitors are doing, let’s take a closer look at some valuation metrics.

Valuation

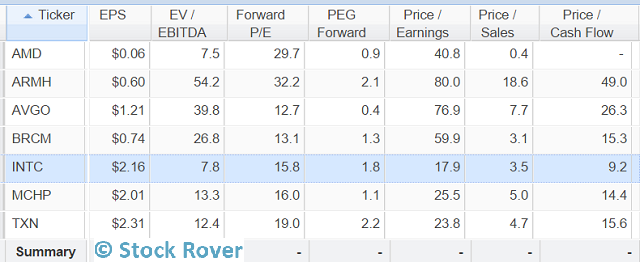

Here is a table of Intel and competitors with a few different valuation metrics:

Intel’s Price / Cash Flow is in the upper spectrum when compared its peers. This gives Intel more room to invest in its business and generate a significant dividend for investors. Intel’s dividends have advanced 450%in the past 10 years, but still are comfortably below half of its projected earnings and Intel recently announced in November that it will increase its quarterly dividend payout from 22.5 cent to 24-cent, a 7% bump.

Intel can plow the remainder of the cash flow back into the company for more growth, which it is currently doing through heavily investing in R&D to keep its competitive edge as the market leader.

Intel is significantly undervalued when looking at it from an EV/EBITDA standpoint, as it is among the lowest within its peer group, only beat out by a declining AMD. Its P/E ratio further supports this line of thinking as it indicates that INTC may be a less expensive stock that is trading at a significant discount to its peers.

Looking at Intel’s predicted future performance, we see that its forward P/E is lower than its current P/E, so earnings are expected to grow. When compared to its peers, Intel’s forward P/E is not the lowest, but it is still quite reasonable. Intel’s PEG forward trades at a premium relative to its peers, but I believe this is justified by the greater overall strength and dominance of the company relative to its more risky peers.

Moving back into a more current view, let’s look at the companies’ Price/Sales and Price/Cash Flow. Price/Cash Flow is an indicator of the value placed on each dollar of a company’s sales or revenues and an indicator of a stock’s valuation, respectively. Intel is trading at a huge discount relative to its peers in both these areas, which is a positive note as low Price/Sales and low Price/Cash Flow means that Intel is trading at a discount and may indicate possible undervaluation.

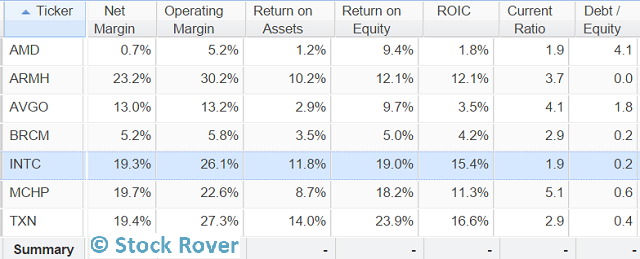

Let’s also take a look at Intel and its competitors from a profitability valuation standpoint:

The first thing to notice should be Intel’s net margin and operating margin, which is in the upper end of the bracket, but still trails behind some of its competitors. Its margins, however, are made up for through its extremely high ROA, ROE & ROIC, which are only bested by Texas Instruments (TXN). This indicates that the company is efficiently run. Intel’s income statement further supports its profitability ratios as its revenue has been on a positive trend in the last 10 years, with its EBITDA margin standing at a whopping 42.1%, beating out the rest of its competitors by a landslide.

Additionally, Intel’s current ratio of 1.9 suggests that it is able to adequately cover its short-term liquidity needs while its extremely low Debt/Equity ratio is a good indicator of how successful Intel is at managing its debt levels. To further elaborate on that point, Intel’s balance sheet is extremely healthy in that it has consistently maintained a large cash pool and a very good ratio between total assets and total liabilities in the past 10 years.

Conclusion

While Intel is not as strong a buy as it was six months ago when it was hovering around the mid $20s, there is still a lot of upside. Revenue growth in its three main operating segments have performed better than expected and is expected to continue at a steady pace. If you also take into consideration the company’s strong income statement and healthy balance sheet as well its strong dividend, then Intel is a relatively safe buy in the long run and definitely still a good stock for long term value investors.

Top